Alyssa Hodges, CPA •

Do you have business operations in Vermont? The state has recently made some significant changes in how corporations will be calculating and filing their taxes. These changes will be effective for the tax year beginning on or after January 1, 2023.

What’s changing?

Do you have business operations in Vermont? The state has recently made some significant changes in how corporations will be calculating and filing their taxes. These changes will be effective for the tax year beginning on or after January 1, 2023.

What’s changing?

As per S.B. 53, the bill links Vermont’s income tax codes to the Federal income tax codes as of December 31, 2021. Changes include:

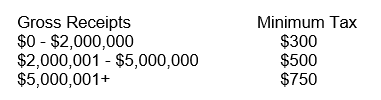

Changes to the Corporate Minimum Tax — Under previous Vermont tax law, a corporation with no (or negative) taxable income was subject to a three-tiered minimum tax based on gross receipts.

Changes to the Corporate Minimum Tax — Under previous Vermont tax law, a corporation with no (or negative) taxable income was subject to a three-tiered minimum tax based on gross receipts.

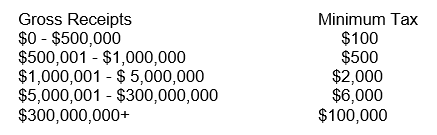

Under the new law, there are five different tiers. The largest corporations will see the most significant jump in their taxes — $99,250 — and businesses with gross receipts less than $500,000 will save a little. The new tax structure applies to C-Corporations, which are also subject to tax rates based on net income.

Changes to Vermont’s Apportionment Formula — Under previous Vermont tax law, the portion of any multi-state corporation’s net income that is pertinent for Vermont taxation was determined by using a three-factor (property, payroll, and double-weighted sales) formula. The new law changes that apportionment to single-factor: sales-only. From now on, a company's net income considered relevant for Vermont taxation is determined by a ratio of the Vermont sales to national sales. This change is expected to benefit corporations with large payroll and property presences in Vermont that also export most of their sales.

This change brings Vermont in line with most other New England states. The only remaining New England state using a three-factor apportionment formula is Massachusetts — although single-factor apportionment is allowed in Massachusetts for certain types of businesses.

Repeal of Throwback Rule — Under previous Vermont tax law, if a corporation sold into a state where it had no nexus, the corporation had to count those sales as Vermont sales to determine their sales apportionment factor. The new legislation repeals that rule.

Questions?

If you have questions about how these changes will impact your future corporate tax filings — or any concerns about your corporate taxes — don’t hesitate to contact Mason + Rich for assistance.

This change brings Vermont in line with most other New England states. The only remaining New England state using a three-factor apportionment formula is Massachusetts — although single-factor apportionment is allowed in Massachusetts for certain types of businesses.

Repeal of Throwback Rule — Under previous Vermont tax law, if a corporation sold into a state where it had no nexus, the corporation had to count those sales as Vermont sales to determine their sales apportionment factor. The new legislation repeals that rule.

Questions?

If you have questions about how these changes will impact your future corporate tax filings — or any concerns about your corporate taxes — don’t hesitate to contact Mason + Rich for assistance.

RSS Feed

RSS Feed